GameStop, and the Politics of Nihilism

Why Fighting "The System" will never work

Quick Follow-Up on Vaccines

Yesterday, in my post about vaccines, I mentioned that the Johnson and Johnson vaccine could soon be available. Well, this morning, the results from its phase 3 trial were released, and it appears to be 66% percent effective against COVID, 72% effective in the US trials:

Data on a vaccine developed by Novavax, who also released results, finding that the vaccine was 89% effective in their UK phase 3 trials.

There was good and bad news contained together in these releases. The bad news is that the topline numbers were not as good as hoped for overall for the Johnson and Johnson vaccine. The trials done in South Africa were the most discouraging, confirming that the new variants of COVID-19 have become more resistant to the vaccine. The South Africa variant of COVID is now in the US and probably will spread farther and faster before this is all over, making our vaccination process more difficult.

The good news is that even with the disappointing topline numbers, the vaccine was still very beneficial. Even with the reduced effectiveness at preventing illness, the vaccine was still very effective in preventing severe disease. Not a single person who got the Johnson and Johnson Vaccine was hospitalized or died. Even if the vaccines do not work correctly against these new variants, getting vaccinated is still a far better option for the alternative, especially given that companies will build booster shots to protect against the variant.

The biggest takeaway is the reminder that speed is essential. The longer COVID is allowed to incubate in our bodies, the more opportunity it has to keep mutating, and the less likely we are to eradicate it. While it appears that COVID is unlikely to mutate as fast as the flu does, it seems like the consensus is that the speed of the vaccination process may determine whether that happens. The fact that a significant portion of the population (probably 30-40%) is still vaccine-hesitant has the potential to lead to a more protracted, messier battle to eradicate COVID.

The speed with which the FDA can conduct its review process and approve these vaccines also is going to be vitally important:

The Great Gamestop Civil War

This week has been a wild one in the financial sector. For those who have not been following, there has been a coordinated effort by a bunch of day-traders on Reddit (a subreddit called “WallStreetBets”) to buy the stock of languishing video game retailer “Game Stop,” and in the process, screw over several hedge funds that had taken a “short” position on GameStop. The Redditors were wildly successful, with GameStop’s stock shooting through the roof, and at least one hedge fund needed a bailout. Yesterday though, it seemed to all come crashing down, as the trading app Robin Hood ran out of the cash they are legally required to keep on hand and stopping processing stock options of Game Stop (and selling positions that traders had bought on margin from the company). Trading has since resumed, and Gamestop is still trading at an outrageous price that will eventually come down. The fallout of this craziness is already evident: there will be an SEC investigation, wild conspiracy theories are spreading, people on both sides of congress are grandstanding, and Elon Musk is a crazy person. Yeah, maybe this is not as unprecedented as it sounds.

I will not attempt to explain this news event (or short-selling) to you, because frankly, others can and have done it far better than I have:

However, I do think it is worth making a few points though:

1) I am not a financial advisor, though I have done a fair amount of work in and around finances, and I have personally read a lot of financial advice. And one of the most significant agreements between different philosophies is this: you should not do amateur day-trading. Warren Buffet gives the investment advice: “Do not invest in what you do not understand.” The vast majority of people will not ever have the expertise to beat the market. To the degree that the Game Stop saga may be a case where some day-traders came out on top (and I do not think that is what is happening), ordinary people will lose their shirts:

If GameStop is overvalued by $20 billion right now, that's $20 billion of losses waiting to accrue, largely to ordinary investors who got caught up in a fad. And while some of the more online traders have gotten cheered for buying at the top by their internet friends, this is far from a desirable democratization of Wall Street — this is just a new way for regular people to lose their shirts.

2) Robin Hood's behavior in all of this is also not proof of economic collusion against the little guy (click on the thread below if you want to understand the underlying mechanics):

HOWEVER, it is proof that you should be very careful about who you trust with your money and skeptical of people who promise you a deal too good to be true. As my friend (and blog reader) Kyle pointed out to me, Robin Hood has a business model with incentives that are terrible for most traders on the app:

Investors aren't Robinhood's customers. Instead, the company sells its order flow, or information about the transactions of its customers, to third parties. Those third parties are the ones who execute the trades, but they also get access to the data.

That can be very valuable to high-frequency traders who make money off the tiny spread in pricing during the time between buy and sell orders. Making even a penny or two off of enough trades every day is real money.

By selling your data in real-time, Robin Hood ensures your decisions can be exploited by professional traders on the other side of the transaction, making each of your trades a fraction less profitable. Finance is all about exploiting mispricing of assets, even if that mispricing is on the margin.

3) The fact that professional investors come out on top when trading with amateurs is not a sign that the economy is necessarily rigged against ordinary people. Inequality is fundamentally different from “rigged.” One can recognize that basketball is rigged because LeBron James would beat all of us in a game of 1-on-1. It is just a fact of life in a specialized economy that if you are not going to be an expert in a narrow field, you will likely lose in a 1-on-1 battle against that expert. The difference is that LeBron does not spend his career traveling to local festivals and beating helpless saps in games of 1-on-1 basketball. In contrast, finance does allow this behavior to happen.

4) I shed no tears for the hedge funds that lost money on their short-selling (and neither should you). But the idea that short-sellers are somehow inherently evil is a silly take. It was rightfully a scandal that companies We Work and Theranos raised billions of dollars from private investors, only to prove worthless scams that somehow went unnoticed. It is an excellent service to the public that investors have a mechanism (short-selling) to alert the general public that a company is overvalued. Our financial system needs healthy conflict and competition to work the same way sports need competition to see athletes perform their best. That may not always feel pleasant, but it is necessary to smoke out bad behavior by companies.

5) If you are depressed that you cannot beat professional traders in day-trading at their own game, I have great news for you: you can beat them by not playing their game. Jack Bogle, the late CEO of Vanguard, invented a great little tool called the “index fund,” which has historically proven to beat almost every active trader around. In the words of my friend (and blog reader) Brandon: “you know who stuck it to the financial man, Jack Bogle.” If folks are looking for simple investing advice to leverage this technology to beat the experts, I will refer you to this little book, which distills investing advice to this:

Start by saving 15 percent of your salary at age 25 into a 401(k), an IRA, or a taxable account (or all three). Put equal amounts of that 15 percent into just three different mutual funds:

A U.S. total stock market index fund

An international total stock market index fund

A U.S. total bond market index fund.

Over time, the three funds will grow at differnet rates, so once per year you’ll adjust their amounts so that they’re again equal

If you want straightforward advice that can apply to finances outside of investing, I will refer you to Harold Pollack, who distilled financial advice into nine rules:

Strive to save 10 to 20 percent of your income a month.

Pay your credit card balance in full every month.

Max out your 401(k) and other tax-advantaged savings accounts (if you have them)

Never buy or sell individual stocks.

Buy inexpensive, well-diversified index mutual funds and exchange-traded funds (and hold onto them over time.

Make your financial advisor commit to the fiduciary standard.

Buy a home when you are financially ready.

Hold Insurance. Make sure you’re protected.

Do what you can to support the social safety net.

I do not think all nine rules can or should be rigidly 100% followed for everyone (many working-class folks would struggle to save 10-20% of their income!). Still, they are pretty good advice for most people to try to follow aspirationally.

The Culture of WallStreetBets

I think it is worth diving into how popular media is portraying WallStreetBets. For instance, here is an article by Jeremy Soane on the culture of the subreddit:

The basic surface-level story of WSB is this. It’s a bunch of autistic losers that live in their mom’s basement who are gambling what little money they have to try and become rich to live lifestyles of hedonism. Since they are basement dwellers their obvious food of choice is chicken tenders aka tendies that they trade in their GBPs (Good boy points) to their mom so they can get more. In this world, they earn good boy points by doing well at stocks.

On the surface, it seems really weird but it’s mostly a type of gallows humor that permeates a lot of especially young millennials and zennial men. That nothing really means anything, that no one cares about them (or in some cases actively hate them), and so they reject buying in on the society they feel actively scorns them. I’ll resist the urge to add my personal opinions or quote Fight Club here, but I’m mostly saying all this to get you in their head.

Soane then tunes to what he believes to be the structural issues that underlie the culture:

See back in the day if you played the rules, worked the job, saved the money you could mostly live a pretty good life. The system was there and it had your back you just had to play by the rules. At some point that changed. Understanding that fundamentally you can do “everything right” and be totally fucked anyways, never able to achieve your dreams regardless of what you do or don’t do is a shitty feeling. Along comes WSB.

Suddenly, there’s a chance. Not a big one, but a chance to get out of your situation and live the life you want. You can do everything right and never be able to retire anyway, OR you can take super speculative positions in the stock market by making giant bets on risky options that, if you happen to be right, could make you rich. You’ve broken the cycle and you can live the life you want. Worst case? You’re right back where you started.

Now, I do not believe this portrayal is 100% accurate. It is widely speculated that a small group of very savvy financial traders on WallStreetBets got into the GameStop position early. They then used the rank and file of WallStreetBets to assemble an army of people to pump up their trades and then dump before the price comes crashing down, leaving them holding the bag. If true, this scheme is probably not illegal, but highly unethical:

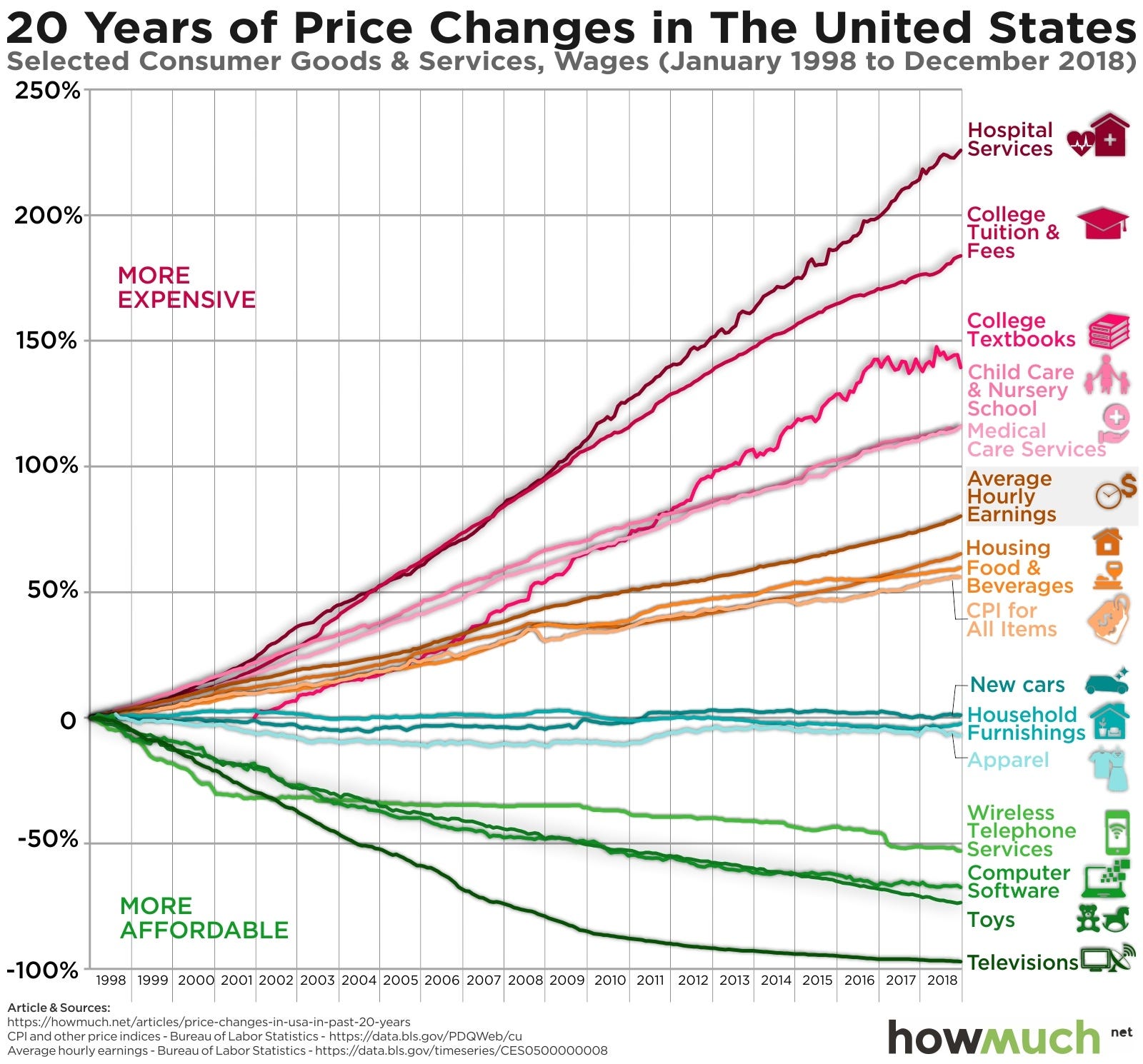

But I think Soane is largely partially right in his description of many of the rank and files guys in this culture. I have known and met young men attracted to day-trading, and while some of it is just “fun,” I think some of it also comes out of this kind of nihilism about the economy and their future. There are many reasons to think that young men's economic prospects are not as good as we would like them to be. For instance, the last 40 years, while seeing tremendous social improvements on many fronts, have seen the cost to consumers go up tremendously in some sectors:

As you can see, the cost of healthcare, education, and housing (which would be even higher if it graphed just cities with good jobs) has gone up astronomically. These are all sectors that you can not merely opt-out of if you want to be a full participant in economic life! Everyone needs a place to live, an adequate education, and everyone faces unexpected medical problems from time to time. These incredibly high prices are especially a problem for people from marginalized backgrounds, who have almost no family safety net. I think this is a real problem in society that we should seriously try to address!

Against the Politics of Doom and Apocolypse

There is a big difference between saying that our economy has specific, concrete inequalities and policy challenges versus saying that the “economy is rigged” and that “you cannot do anything to get ahead.” Why? Well, I think there is a convincing case you can look at the political controversies of the last five years or so and see how American politics has increasingly become the politics of apocalyptic doom. I think this is illustrated by how many advocacy efforts (on both sides of the aisle) have gone in recent years:

Did telling people that COVID is so contagious that people can’t leave their house (rather than focusing on risk mitigation measures) lead to increased compliance with guidelines? It seems that it led to more people “giving up” and trying to live a normal life with no precautions.

Is focusing people on COVID vaccines’ imperfections (instead of their strengths) making people follow guidelines? It seems to me it just makes people less likely to get the vaccine.

Does Donald Trump telling people that last november’s election was stolen help the GOP win a special election in Georgia? It seems to me the rhetoric fed into the GOP’s loss in Georgia by alienating moderates and justifying crazy people to storm the capitol.

Did Trump’s apocalyptic rhetoric about immigration lead to reforms of the immigration system? Instead, it seems the cause of allowing more immigration to get more popular with the American public.

Does telling people that climate change is a looming apocalypse lead to personal behavior changes and increased support for mitigation measures? It seems to me its instead leading to suffer from childhood anxiety and focus on the need for vague structural change over an above specific effective policy (like a carbon tax)

Likewise, people who come to believe the economy is rigged do not become organized advocates for economic reform to make housing, healthcare, and education more accessible. They instead become nihilists day-trading on WallStreetBets:

The problem is that the rhetoric of doom does not work in politics. Politics works on the logic of incremental reform by building support for concrete policies, often a long and slow work. Doom makes us give up on that hard, slow work of reform before achieving our goal.

The problem is not that our economy is “broken” or “rigged” in some abstract way. Instead, we have failed to identify and implement policies that make life better for working people. It makes far more sense to improve housing, healthcare, and education than to focus on the financial sector. And if you want to stick it to big finance, there are plenty of practical policies that can make the finance sector more competitive and less prone to self-dealing and excessive leverage.

A Better Economic Story

We should be telling a more precise, more nuanced, yet also more hopeful picture of personal finance in our economy today:

We live in a world where many structural factors have made it harder to achieve a middle-class lifestyle in America, especially for people from marginalized backgrounds. Some of this lies at the feet of public policy—some at the feet of shrewd business accounting that noticed that defined pensions were a considerable risk. But it is a fact we have to deal with

At the same time, individual choices about work, education, and marriage can make it a lot easier to achieve good life outcomes. Just because it is hard to muster up the personal discipline to gain job skills, save your earnings, and invest in low-cost index funds, does not mean it is impossible.

Given the reality of #1 and the fact that this is financial advice that is hard for most human beings to follow, and so we as a society should advocate for specific and reasonable policy reform that makes it even easier to live a middle-class lifestyle

And ultimately, it is worth noting that in America, we also have a very narrow, individualistic way of looking at money as a private and personal responsibility. One does not need to be an economic collectivist to think that bringing a community of trust into your finances is a far better way to approach it in the long-run. A community can hold us to hard commitments, a community can push us towards better choices, and maybe most importantly, can help us see that getting rich is not what ultimately matters. Most of us are far happier with a certain level of economic security, far less than what we might think. And being generous, another aspect of the financial community is even better at making us happy. These are wise insights that religious communities have known for centuries, and I hope that contemporary secular communities will rediscover as well.