As you probably have heard, Joe Biden has devised a plan to cancel $10,000 of student debt and $20,000 for those with Pell Grants. There is an income cap of $125,000 for individuals and $250,000 for households. There are a lot of unknowns in how Biden will implement forgiveness, the biggest of which is whether it will be held up in court and ultimately be found unconstitutional:

It is disappointing to see the ongoing trend of presidents pushing the boundaries of their executive power in ways that do not fall into the discretion that congress meant to give them. Ultimately, fixes to the student loan program, especially those with budget implications, should happen through congress, not the president. Unfortunately, EVERY recent president has increasingly done this to get around gridlock in congress (Trump and Obama both did this, especially on immigration). This is a downstream consequence of polarization: if congress does not compromise and legislate to solve issues, the president will come under pressure to "just do something." Even though the solution does not truly solve real problems, the president's having "done something" is enough to give congress the cover not to address the issue for an even more extended period and instead play to their base.

Regardless of those details, I thought it was worth returning to the case I made against student loan forgiveness a few months back. If you want to read that in full, you can do so below:

The thesis of my arguments was this:

Student loan forgiveness is trickle-down economics dressed up in progressive clothes, and large-scale forgiveness would be a large-scale disaster for economic equality — especially in my home state of California.

Student loan forgiveness is very regressive. Only ~33% of Americans have a bachelor's degree, while an overwhelming number have never finished college. Thus, student loan forgiveness disproportionately benefits a small minority of Americans. In addition, that small minority is not the most economically needy:

The Brookings Institution has found that only 2% of student debt is owed by those in the lowest 20% of earners. After all, those who make the least amount in the labor market tend to have not attended college. On the flip side, approximately two-thirds of college debt belongs to borrowers in the top 40% of income earners. The same analysis found that college debt holders are significantly better off than those who own mortgage debt. Many large borrowers went to elite private undergraduate schools; others went to professional graduate schools. A full 10% of student debt is held ONLY by doctors, lawyers, and MBA grads. No one thinks these are truly disadvantaged in our society. So why are we considering bailing them out?

The Brookings analysis shows how the usual way of analyzing student loan burdens (assets without human capital, shown in blue) instead of the more precise method (income, shown in gray) widely skews the perception of who is in need:

While Biden tried to avoid this mistake through means testing and forgiving only $10,000 in debt per borrower, the program will still be regressive. Wharton’s federal budget model found that even the current design of the bill is still regressive. The quintile benefitting the most will be the 60 to 80 quintile, who would receive 27% of the benefits.

As Wharton says, this model also doesn’t account for the ways in which forgiveness might create incentives for students to borrow more, and incentives for colleges to raise prices going forward:

If student loan debt forgiveness is ongoing, students might eventually reorganize their financing toward additional borrowing. Moreover, more students might choose to attend qualifying education providers, including students who might otherwise have a harder time with repayment. The inclusion of these two effects could, to some extent, make the program a bit more progressive while increasing budgetary costs. A third effect could also emerge: some of the benefit from debt forgiveness might be captured by colleges themselves in the form of higher prices (both tuition and net).

Student Loan Forgiveness is Terrible Prioritization

While Biden tried to avoid this mistake through means testing and forgiving only $10,000 in debt per borrower, the program will still be regressive. Wharton's federal budget model found that even the current design of the bill is still regressive. The quintile benefitting the most will be the 60 to 80 quintile, which would receive 27% of the benefits.

As Wharton says, this model also doesn't account for how forgiveness might create incentives for students to borrow more and incentives for colleges to raise prices in the future:

If student loan debt forgiveness is ongoing, students might eventually reorganize their financing toward additional borrowing. Moreover, more students might choose to attend qualifying education providers, including students who might otherwise have a harder time with repayment. The inclusion of these two effects could, to some extent, make the program a bit more progressive while increasing budgetary costs. A third effect could also emerge: some of the benefit from debt forgiveness might be captured by colleges themselves in the form of higher prices (both tuition and net).

Student Loan Forgiveness Shows Terrible Prioritization

The "Inflation Reduction Act" (IRA) was recently passed in Congress. Its final form is a mix of tax increases and decarbonizing incentives. We have yet to see the impact of the IRA on inflation (probably little) or climate (it could be significant). However, many left-of-center people have already cheered its passage as a big win. If you are one of them, you should consider that student loan forgiveness will likely increase inflation by far more than the IRA decreased it. The cost of student loan forgiveness, estimated by some to be about $300 billion, is likely almost as much as all the climate investments in the IRA (estimated to be about $370 billion)

I don't think the climate investments in the IRA were ideally structured, but at least they had a worthwhile intention: keeping future generations from worst-case climate scenarios. What is worse is that the IRA at first was pitched as Build Back Better (BBB) and originally included a series of social safety net programs directed at parents. I thought the original BBB had fatal flaws, especially regarding its childcare proposal. Still, the idea that there was a need to offset the costs of raising children was worthwhile, as I wrote in February of 2021:

Now, the child tax credit was stripped out of BBB because Joe Manchin was skeptical of elements of the program and was concerned about inflation. However, the expanded Child Tax Credit (CTC) would have only cost $160 billion per year compared to the $300 billion that student loan forgiveness will cost. Even better, Mitt Romney has a plan to permanently expand the CTC without increasing the deficit. Furthermore, studies show that investing in children by giving their parents tax benefits and cash support pays enormous dividends. One recent study found that lifetime earnings for kids in the programs increased by 1-2 percent yearly. It doesn't sound like much, but it is more than enough for the program to pay for itself in future tax revenues. When parents received the money, boys saw even more significant impacts on their future earnings, increasing 2-3% yearly. These results outstrip those of the famed Perry pre-school program, but with the added benefits of the results being found at scale (something Perry has never been able to do). And this is not an outlier: repeatedly, studies show the social safety net programs that help poor kids have a very high return on investment.

So, while the CTC, a program that could be expected to make a difference in child poverty, was sacrificed on the altar of prioritization and inflation, student loan forgiveness survived. So congrats, over-educated folks on Twitter; you made enough noise to get your needs prioritized over poor kids.

What are we trying to solve?

But the real problem with student loan forgiveness is that it is not nearly ambitious enough to tackle the root problems. It doesn’t help current low-income kids attend college, and it will make inflation worse. Does loan forgiveness reduce the massive cost issue in higher education? Not at all; forgiving loans does nothing to drive down future costs, in fact universities are likely to start marketing the potential for future loan forgiveness as a way to cover their tuition increases.

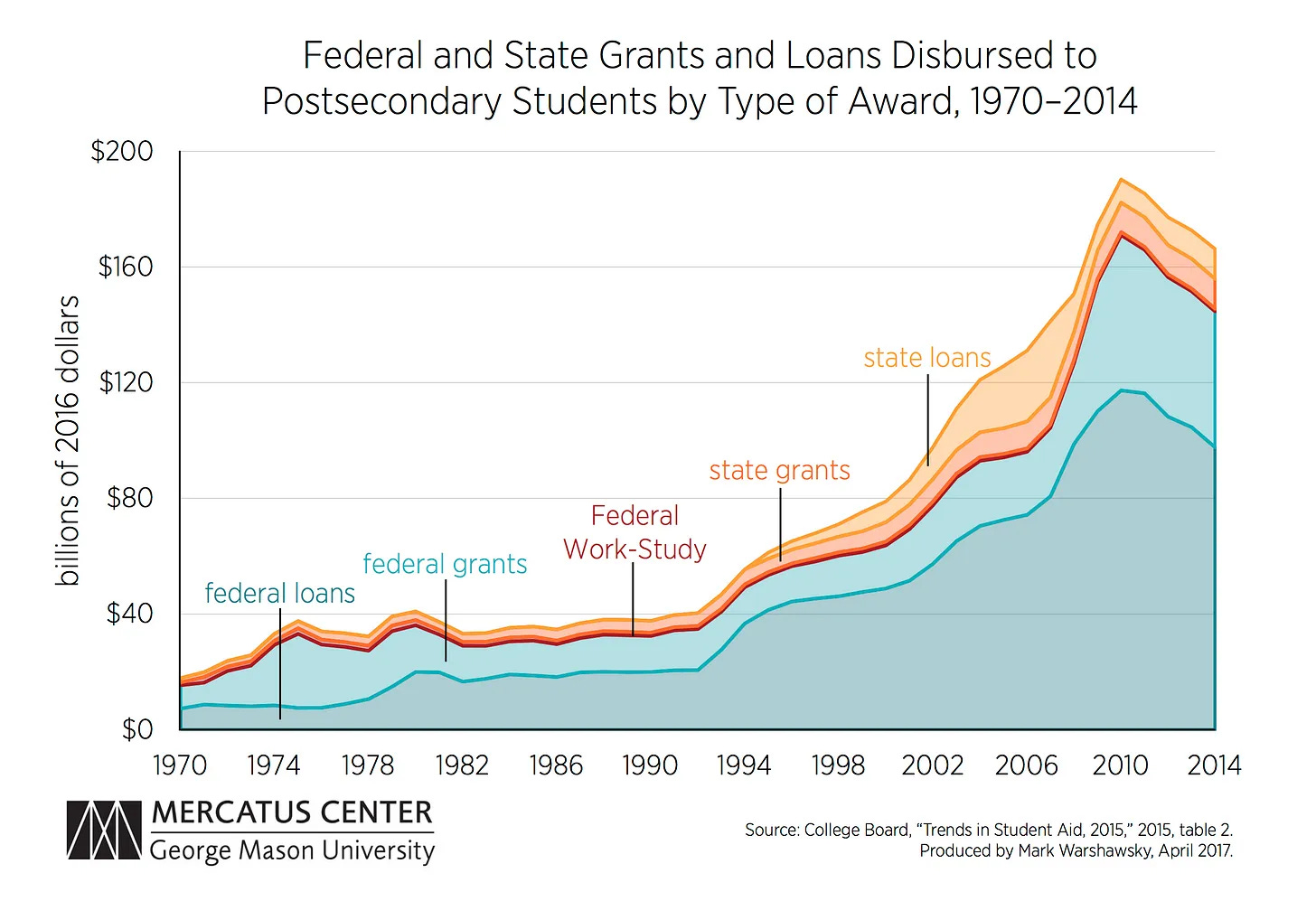

If we want to see improvement, we need to find ways to supply more and better education at lower prices. I have argued before with housing that when you increase subsidies in a supply and productivity-constrained environment, you simply see prices go up, and those subsidies are captured by existing property owners. College is no different: we have seen stagnant productivity, a flat supply (especially at elite colleges), while there has been a massive uptick in cheap student loans:

Studies have shown that these cheap, subsidized loans lead directly to higher tuition prices. Thus, tuition at US universities is about double the tuition in other wealthy nations ($31,600 vs. $16,200 per year in the OECD average). A massive amount of this additional cost is spent on fancy buildings and increased administrative costs, which is of dubious educational value to students:

For higher ed to actually see reform, we must do what we can to reverse this "cost-disease" while increasing quality. This is a difficult task and something no one knows how to do quite yet. I have some ideas, which I will outline in a future post. There are many promising initiatives in higher education. The widespread proliferation of online classes on platforms like Coursera and EDx has not disrupted higher education as they promised. Rather, they have provided value as alternatives to graduate school for professionals looking for practical skills. In the job training space, Ascent Funding is working to identify worthwhile job training programs (including coding boot camps) and offers private loans to students to learn skills that will have high ROI in the future. As far as curricula, my friend Ji is working to standardize a statistics curriculum through an effort called CourseKata. They use real-time data on what material is working to innovate and change the curriculum. If this initiative works, it could increase the quality of education at a lower price point. Creating a standardized and well-designed curriculum could substitute capital for labor and make higher education less dependent on the limited supply of "experts" to be teachers. Yet all these innovators are not rewarded by loan forgiveness; instead, the current system gets a massive implicit subsidy to traditional higher education with no strings attached.

As a personal example, I recently applied to a new model of MBA program called Quantic, which aims to deliver business education at a significantly reduced price ($10,000 for an MBA instead of $100,000). I was drawn to Quantic because if their model is successful, it could substantially democratize graduate school. Will it work? No one knows for sure. However, since I have been accepted, I am considering trying it. We need risk-taking and innovation in education. I have no desire to spend $100,000 on a graduate degree, only to return to work in an organization that believes in living simply in solidarity with the marginalized. But hey, it would be nice to have some quality continuing education and an advanced degree at a reasonable price, especially since all my friends seem to be getting them! The problem is, to try to build an innovative model, Quantic works outside of the federal student loan program, and students working outside of the student loan program get no benefits from the Biden action.

Meanwhile, most traditional higher education is adapting far too slowly. As Noah Smith points out, starting in about 2006, there was a massive decline in the number of jobs looking for students with a humanities background:

Smith points out that this crash corresponded with a stagnation in the number of jobs in law, teaching, and government, all of which were careers humanities majors could fall back on. It also coincided with a decline in tenured positions opened in academia as older faculty refused to retire. Finally, given the crash on Wall-Street in 2008, there were also fewer finance jobs available to humanities majors than ten years before. The finance jobs that survived the crisis went to more quantitatively skilled students.

Now I am not against humanities majors: I was one myself. But universities saw the number of humanities majors increase well into the 2010s, even as the job market was disappearing:

Universities did not pivot and set their students up for success. Universities could have found ways to ensure that their humanities majors also had practical skills. For example, data science and analysis were booming in the 2000s and the 2010s but were not widely incorporated as a discrete area of study at colleges until the late 2010s.

The real problem was at the graduate level: many universities still offer economically useless master's degrees in the humanities and charge a fortune for them. Columbia University charges their film graduate students so much that they graduate with a median debt of $181,000, then make less than $30,000 a year. This is predatory behavior, and Columbia is being bailed out by student loan forgiveness. Columbia should be ashamed of what they are doing, but they are rewarded, not punished, by federal programs. What kind of incentive is that for innovation? Zaid Jilani put this paradox well:

Unless we solve these fundamental systemic problems in higher education, we will force future generations to go down the same ruinous path.