Why California shouldn't give me money to buy a House

My Case in the Washington Post Against Homeownership Subsidies

My latest op-ed was published today in the Washington Post, where I try to outline a case against California’s new program to subsidize would-be first-time home buyers in California (like myself). You can read the full op-ed here (clocking in at a breezy 800 words), and please click, read and share widely!

But after you read the piece, I thought I would use this blog to add a little flavor and context for those interested more!

The context of the article is simple: California has a deep and growing housing crisis, which has a significant impact on people across the income spectrum:

At this point, few people would dispute the idea that California has a severe housing crisis. With more buyers than available supply, the median home price is $898,000. Rent for a three-bedroom house is more than $3,000 a month. Many families like mine — hoping to stop renting and buy our first home — are feeling desperate.

It was tempting to celebrate news late last month that the state legislature had passed a budget that included half a billion dollars for a program providing down-payment assistance for first-time home buyers. But the well-intentioned legislation, as is so often the case with policies throwing money at problems, may end up doing more harm than good.

The “California Dream for All Program” would lend qualified middle-class Californians up to 17 percent of a home’s value for their down payment. Sounds good. If my family were lucky enough to be one of those funded through the program, it theoretically could provide just enough assistance to help us break into the housing market.

When this program was first introduced into the senate, I saw people I know who are not ordinarily plugged into the housing conversation excited about this program (which was initially supposed to cost over 1 billion but was later trimmed down to 500 million). That is because home ownership is widely popular in America: there is a deep-rooted sense you can address economic opportunity by helping people buy their own homes. Classic movies like Its a Wonderful Life forefront this notion, as did the Bush Administration with its “Ownership Society” messaging.

The problem is that there is a long body of economic research detailing what happens when you subsidize homeownership, especially in supply-constrained environments: homes simply go up:

The more likely scenario: With more money in the real estate market but not enough houses, prices will rise. The down-payment help would enable my family bid on a house, but we’d be in no position to compete with anyone who wants to outbid us. And that’s exactly what happens when there aren’t enough houses available.

The big winners of subsidies will ultimately be existing homeowners, who will naturally seek the best price.

That’s a crushing realization for my wife and me. We live in East Los Angeles and have spent the past four years saving as much as possible to enter the housing market. We’re both college-educated and work nonprofit jobs that, while not highly lucrative, would have provided enough for a modest home just a decade ago. But it seems no matter how much we save, prices steadily climb beyond our budget.

I am a broken record at this point, but you cannot deal with the problems in housing unless you deal with supply! In the last 50 years, California has added 6.7 million households and 19 million people, but only 6.2 million homes:

In March, the California Department of Housing and Community Development said 2.5 million new homes would need to be built by 2030 to address a housing shortfall that has been half a century in the making.

Over that span, ever-tightening zoning regulations have choked off housing options for countless middle-class families. Townhouses, duplexes and small apartment buildings are widely banned — including on 75 percent of residential land in Los Angeles and 94 percent in San Jose.

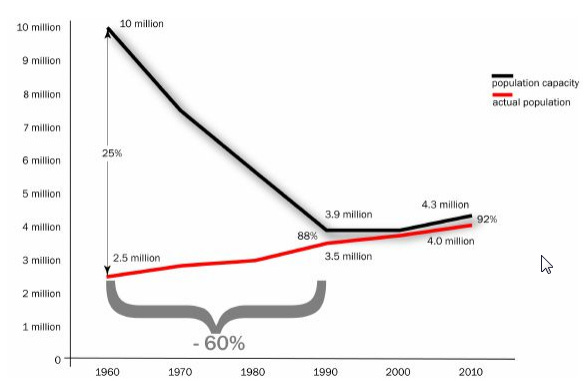

To help illustrate how this shortfall has its roots in zoning comes from a useful graphic created by Greg Morrow in his urban planning dissertation at UCLA:

1960, when LA had about 2.5 million residents, our city’s zoning plan allowed for up to 10 million homes to be built. This “zoning buffer” meant that anytime prices rose and demand for housing went up, developers could build more to satisfy that need. However, over the following decades, LA was downzoned, especially along commercial corridors. As a result, by 2010, the zoned capacity for the city was only 4.3 million homes, even though the population had gone up to 4 million.

Maintaining healthy “zoning buffers” alone does not instantly build housing, but they create the conditions for developers to build out the needed supply over time. Shane Phillips, who is a housing policy guru over at UCLA (and fellow Eastside resident), illustrated on his blog the impact this had on housing development in the city of LA:

If you are interested in more, you can go back and read a post from last year about the urgent need for zoning reform:

But the topline takeaway is that until the state can build more housing, we aren’t seeing a family’s economic prospects improve. As I write in the piece:

State lawmakers periodically try to attack the problem at its root, but ambitious bills that would address the supply problem have repeatedly died in Sacramento at the hands of politicians fearing retribution from not-in-my-backyard voters. Hence the politically safer but financially dubious move to subsidize down-payments for first-time home buyers.

What was new to me in writing this piece was to dig into the research on how much subsidies for homeownership can backfire:

To assess the prospects of success for the California Dream for All fund consider the effect of a homeowner subsidy already in effect. Research on the mortgage interest deduction shows that subsidizing homeowner’s mortgages pushes up the cost of housing because buyers can afford to pay more for their houses.

The deduction does not make homeownership more accessible; it often prices lower-income buyers out of the market, while better-off homeowners disproportionately use the benefit simply to buy larger homes.

When economists Sommer and Sullivan modeled the impacts of the mortgage interest deduction was pretty shocking: they found that the mortgage interest deduction would be a net benefit to almost everyone except the wealthiest Americans:

The model demonstrates that repealing the regressive mortgage interest deduction decreases housing consumption by the wealthy, increases aggregate homeownership, improves overall welfare, and leads to a decline in aggregate mortgage debt.

This is not an isolated study either: 85% of economists, when polled, think the market would be better off without the mortgage interest deduction.

To clarify, I am not saying all subsidies always do more harm than good. There is an appropriate place for targeted and temporary relief to those suffering the most in a crisis. But it is essential to recognize that such actions can have unintended consequences, which will make things worse if you do not also treat the root causes. Subsidizing homeownership without taking the drastic and necessary steps to increase supply is like taking painkillers to cope with a broken bone that still needs to be set. And most importantly, programs need to be designed to ensure those getting the subsidy are actually in need:

If government is going to subsidize anyone’s housing, it should be those most urgently in need. In California right now, 160,000 people are living without a home, and an additional 1.5 million low-income renters spend over half their income on rent. Renters stretched to paying 50 percent of their income on rent are unlikely ever to afford to buy a home, even with homeownership subsidies.

As much as I’d enjoy government assistance in buying a house, I’m under no illusion that my predicament is as dire as that of someone struggling to keep a roof over their head.

Los Angeles is full of cost-burdened renters. A door-to-door survey of renters in South and Central Los Angeles recently found that during 2019, 73% paid more than 30% of their income on rent, while 48% paid half their income on rent. These were very poor renters, with a median income of $2600/month, leading many of them to cut back on other essentials like food to pay their rent. Overall, Los Angeles renters are the 2nd most cost-burdened (ie paying 30% or more of income on rent) of anywhere in the US.

Few people realize how much housing assistance in contemporary America is skewed towards homeowners, who tend to be wealthier and away from renters. For example, homeowners can deduct mortgage interest and property taxes from income taxes, and primary home sales are exempted from capital gains, which tallied $75 billion in 2019. Moreover, 90% of these tax benefits go to those with incomes over $100,000 a year. Before the Tax Cuts and Jobs Act of 2017, these programs totaled over $130 Billion in federal benefits. And this figure doesn’t even consider all the more hidden subsidies we give homeownership:

Homeowners don’t get taxed for imputed rent, which is the tricky but economically sound idea that tax-wise, they get to live in their property for free.

Many homeowners get already get generous assistance from various levels of government with down payments.

All homeowners get indirect assistance through federal guarantees of mortgages, which keeps lending rates lower than they would be.

When you add all of these subsidies together, they dwarf the most significant federal programs that help low-income renters: Section 8 Vouchers and LIHTC (tax credits for affordable housing projects). These two programs combined ran a little over $34 billion in 2019, less than half of just the “on-the-book” federal homeownership subsidy.

In a world of limited resources, policymakers have to make hard choices. One can acknowledge upper-middle-class Californians (including myself) frustrations over the high cost of buying a house while also keeping in mind that they are far from the most housing insecure. In a world of limited resources, policymakers have to make hard choices. One can acknowledge upper-middle-class Californians (including myself) frustrations over the high cost of buying a house while also keeping in mind that they are far from the most housing insecure. I would have much preferred the state fund SB 843, which would increase the renter’s tax credit than give a subsidy to homeowners.

That said, I have written before that subsidies for renters, while good and essential, are limited in what they can accomplish:

This is why the way to move forward is to incrementally chip away at harmful housing and land-use regulations and incrementally build the homes we need for all Californians at all income levels. Increasing the supply of homes will, in the long run, help all people of all socioeconomic backgrounds by ensuring everyone has more affordable options for housing:

Instead of inviting higher housing prices by subsidizing first-time home buyers in California, lawmakers could steel themselves against NIMBY (not in my backyard) resistance and reform at least some zoning laws. A California bill now under consideration would remove parking minimums across the state (requiring a certain number of parking spots is a common way for localities to block construction of denser housing). In 2019, San Diego dropped its parking requirements in areas near transit stops, and saw housing construction more than quadruple.

Another bill would legalize housing in commercial corridors. Evidence from Minneapolis shows that such a move produces more housing and helps bring down prices.

I would love to buy a house, but I would prefer to do it without taking resources that could go to those truly in need. Providing financial assistance to first-time home buyers does nothing to produce more new houses — and building more houses, not just making existing ones more expensive, is the only way California can solve its housing problem.